Statistics released today by the Canadian Real Estate Association (CREA) show national home sales were unchanged from September to October 2019.

Highlights:

- National home sales held steady on a month-over-month (m-o-m) basis in October.

- Actual (not seasonally adjusted) activity was up 12.9% year-over-year (y-o-y).

- The number of newly listed properties declined by 1.8% m-o-m.

- The MLS® Home Price Index (HPI) advanced by 0.6% m-o-m and 1.8% y-o-y.

- The actual (not seasonally adjusted) national average sale price climbed 5.8% y-o-y.

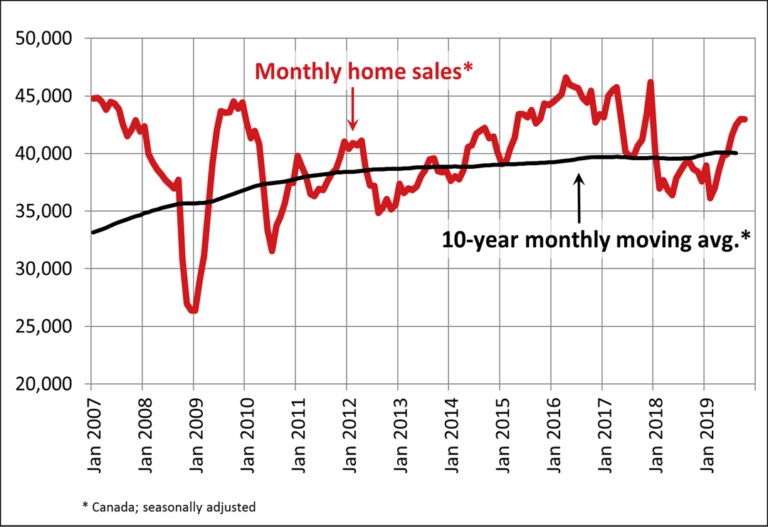

Home sales recorded via Canadian MLS® Systems remained steady in October 2019 following a string of monthly increases that began in March. Activity is now almost 20% above the six-year low reached in February 2019 but remains 7% below heights reached in 2016 and 2017. (Chart A)

There was an almost even split between the number of local markets where activity rose and those where it declined. Higher sales in Greater Vancouver (GVA), the neighbouring Fraser Valley and Ottawa offset a monthly decline in activity in the Greater Toronto Area (GTA)—particularly in Central Toronto—and Hamilton-Burlington

Actual (not seasonally adjusted) activity rose 12.9% year-over-year. Transactions were up from year-ago levels in 80% of all local markets in October, including all of Canada’s largest urban markets.

“Steady national activity in October hides how the mortgage stress-test remains a drag on many local housing markets where the balance between supply and demand favours homebuyers in purchase negotiations,” said Jason Stephen, president of CREA. “That said, all real estate is local, so market balance varies depending on location, housing type, and price segment. Nobody knows that better than a professional REALTOR®, your best source for information and guidance when negotiating the sale or purchase of a home,” said Stephen.

“It’s a full-blown buyer’s market or on the cusp of one in a number of housing markets across the Prairies and in Newfoundland,” said Gregory Klump, CREA’s Chief Economist. “Homebuyers there have the upper hand in purchase negotiations and the mortgage stress-test has contributed to that by reducing the number of competing buyers who can qualify for mortgage financing while market conditions are in their favour.”

The number of newly listed homes fell by 1.8% in October, with the GTA and Ottawa posting the largest declines. Almost a third of all housing markets posted a monthly decline of at least 5%, while about a fifth of all markets posted a monthly increase of at least 5%.

Steady sales and fewer new listings further tightened the national sales-to-new listings ratio to 63.7%. This measure has been increasingly rising above its long-term average of 53.6%. Its current reading suggests that sales negotiations are becoming increasingly tilted in favour of sellers; however, the national measure continues to mask significant regional variations.

Considering the degree and duration to which market balance readings are above or below their long-term averages is the best way of gauging whether local housing market conditions favour buyers or sellers. Market balance measures that are within one standard deviation of their long-term average are generally consistent with balanced market conditions.

Based on a comparison of the sales-to-new listings ratio with the long-term average, just over two-thirds of all local markets were in balanced market territory in October 2019, including the GTA and Lower Mainland of British Columbia. Nonetheless, sales negotiations remain tilted in favour of buyers in housing markets located in Alberta, Saskatchewan and Newfoundland & Labrador.

The number of months of inventory is another important measure of the balance between sales and the supply of listings. It represents how long it would take to liquidate current inventories at the current rate of sales activity.

There were 4.4 months of inventory on a national basis at the end of October 2019—the lowest level recorded since April 2017. This measure of market balance has been retreating further below its long-term average of 5.3 months. While still within balanced market territory, its current reading suggests that sales negotiations are becoming increasingly tilted in favour of sellers.

National measures of market balance continue to mask significant regional variations. The number of months of inventory has swollen far beyond long-term averages in Prairie provinces and Newfoundland & Labrador, giving homebuyers ample choice in these regions. By contrast, the measure is running well below long-term averages in Ontario, Quebec and Maritime provinces, resulting in increased competition among buyers for listings and providing fertile ground for price gains. The measure is still well centred within balanced market territory in the Lower Mainland of British Columbia.

The Aggregate Composite MLS® Home Price Index (MLS® HPI) rose 0.6%, marking its fifth consecutive monthly gain. (Chart B)

Seasonally adjusted MLS® HPI readings in October were up from the previous month in 14 of the 18 markets tracked by the index. (Table 1)

Recently, home price trends have generally been stabilizing in the Lower Mainland and the Prairies. While that remains the case in Calgary and Saskatoon, home prices in Edmonton and Regina have moved lower. By contrast, home price trends have started to recover in the GVA and the neighbouring Fraser Valley.

Meanwhile, price growth continues to rebound in the Greater Golden Horseshoe (GGH). In markets further east, price growth has been trending higher for the last three or four years.

Comparing home prices to year-ago levels yields considerable variations across the country, with mostly declines in western Canada and mostly price gains in eastern Canada.

The actual (not seasonally adjusted) Aggregate Composite MLS® (HPI) was up 1.8% y-o-y in October 2019, the biggest year-over-year gain since November 2018.

Home prices in the GVA (-6.4%) and the Fraser Valley (-4.2%) are still below year-ago levels, although declines are becoming smaller.

Elsewhere in British Columbia, home prices logged y-o-y increases on Vancouver Island and in the Okanagan Valley (3.1% and 2%, respectively) while having edged marginally higher in Victoria (0.5% y-o-y).

Calgary, Edmonton and Saskatoon posted price declines in the range of -1.5% to -2.5% on a y-o-y basis in October, while the gap between this year and last year widened sharply to -6.8% in Regina.

In Ontario, price growth has re-accelerated well ahead of overall consumer price inflation across most of the GGH. Meanwhile, price growth in recent years has continued uninterrupted in Ottawa, Montreal and Moncton.

All benchmark home categories tracked by the index remained in positive y-o-y territory in October 2019. Two-storey single-family home prices were up most, rising 2.5% y-o-y. One-storey single family home prices rose 1.4% y-o-y, while townhouse/row and apartment units climbed by 1% and 1.2%, respectively.

The MLS® HPI provides the best way to gauge price trends, because averages are strongly distorted by changes in the mix of sales activity from one month to the next.

The actual (not seasonally adjusted) national average price for homes sold in October 2019 was around $525,000, up 5.8% from the same month last year.

The national average price is heavily skewed by sales in the GVA and GTA, two of Canada’s most active and expensive housing markets. Excluding these two markets from calculations cuts almost $125,000 from the national average price, trimming it to around $400,000 and reducing the year-over-year gain to 4.7%.

Provided by: CREA