The once bright outlook for the economy, with visions of a second “roaring 20s” fueled by pent-up demand and accumulated savings, has given way to uncertainty and the gloom of a potential recession this year. The shift in outlook was brought on by the monetary policy response to multi-decade high inflation as the Bank of Canada tightened its policy rate at its fastest pace since the 1990s. While we are still waiting on a broader economic downturn, the housing market immediately felt the impact of elevated interest rates.

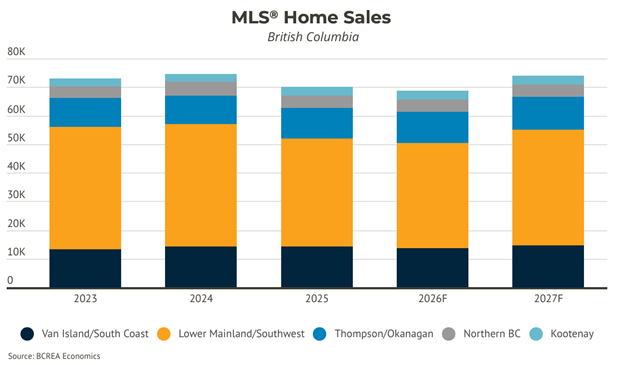

Although the annual level of home sales in 2022 was near its long-term average, that measure masks a radical shift in the market that coincided with the rise of interest rates. Home sales activity declined sharply through the spring and summer months and sales are now trending close to 25 per cent below normal. We anticipate that home sales will remain slow in 2023 as the market continues to be constrained by high mortgage rates and absorbs the impact of a slowing economy. However, the housing market historically tends to lead the business cycle and the onset of recession generally coincides with the beginning of a recovery in the housing market and a substantial rise in activity the following year as the economy heals and the impact of falling mortgage rates unlocks demand. The recovery will be given a further boost as Canada looks to welcome a record 1.5 million new immigrants over the next three years. As such, we expect activity to pick up later this year and strengthen through 2024. That said, sales will be low this year at a forecasted 75,150 units before rising to 93,025 units next year.

With sales down sharply, inventories have accumulated from the severely depleted level at the start of 2022 but remain low by historical standards. However, the abrupt shift in market conditions has meant that prices have come down despite low inventory, falling from peak levels through the spring before stabilizing toward the end of last year. While we expect MLS® average prices to trend relatively flat this year, they will be lower than peak values of 2022. Consequently, year-over-year comparisons will register negative for much of 2023, which will likely result in negative annual price growth even if monthly prices begin to recover as expected later this year.

Provided by: BCREA